The Strait of Hormuz is back at the centre of the market conversation, and this time the story has moved beyond vague geopolitical risk.

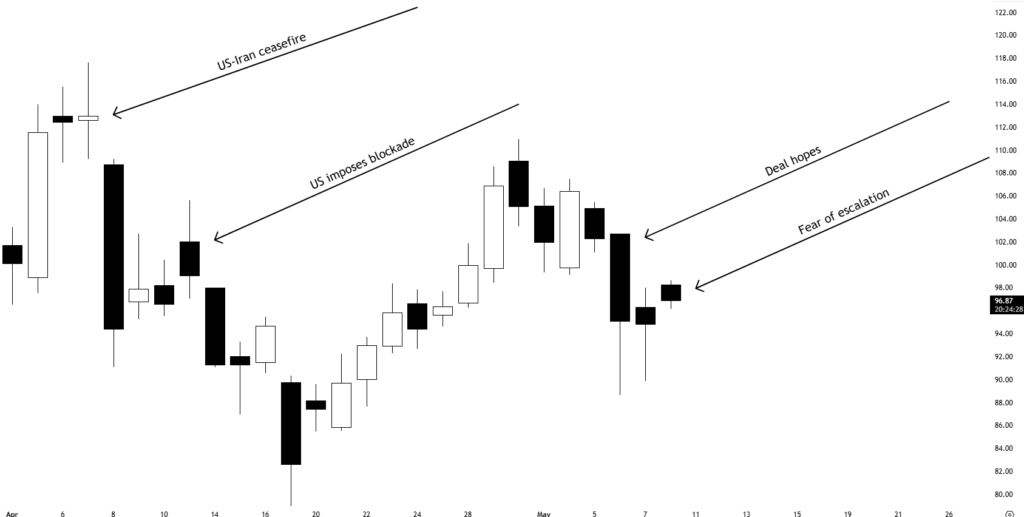

The latest developments suggest the US-Iran ceasefire is under its most serious pressure yet. The US and Iran have exchanged fire around the Strait of Hormuz, Iran has accused the US of striking vessels and Iranian territory, and US Central Command says it carried out retaliatory strikes after Iranian missiles, drones and small boats targeted three US Navy destroyers. Iran claimed it caused “significant damage”, while the US said none of its assets were hit.

That matters because Hormuz is not just a political flashpoint. It is one of the world’s most important energy corridors. Reuters has noted that around a fifth of global oil and LNG supplies normally pass through the strait, which means any serious disruption can quickly become a macro problem, not just a regional one.

For FX markets, this is the kind of story that can shift quickly from “headline risk” to “regime risk”.

At the moment, the market is not treating this as a clean, full-blown risk-off event. But it is starting to price a more fragile backdrop: oil is jumping, safe-haven currencies are back on the radar, and traders are having to think harder about whether this is just another short-lived flare-up or the start of a more persistent energy shock.

The key change: this is no longer just diplomatic noise

Earlier in the week, the market was still trying to lean on the idea that the ceasefire could hold. There was talk of a US proposal to stop the fighting, although Reuters reported that the framework would leave some of the most contentious issues, including Iran’s nuclear programme, unresolved for now.

That has now become harder to ignore.

The newer developments point to three separate pressure points.

First, the US and Iran have exchanged fire again. That alone raises the risk of miscalculation.

Second, the US blockade of Iranian ports remains in place. According to the latest Reuters updates provided, the blockade began on April 13 after Iran halted nearly all shipping from the Strait of Hormuz. The US says it has turned around dozens of ships since then, while Iranian oil exports have reportedly shrunk sharply.

Third, Washington is pushing a United Nations resolution demanding Iran halt attacks and mining activity around the Strait of Hormuz, but diplomats expect China and Russia may veto it. Reuters has also reported that the US-proposed resolution faces likely vetoes from China and Russia, partly because they view the language as biased and politically charged.

So this is not just one military incident. It is becoming a layered problem involving shipping, oil exports, military retaliation, diplomacy, and great-power politics.

That is why FX markets need to pay attention.

Oil is the first transmission channel

The cleanest market reaction has been in oil.

Reuters reported that US crude futures rose as much as 3% after the renewed hostilities, with WTI trading around USD 97.26 a barrel after initially gaining more than 3%. That is the obvious first channel from Hormuz risk into global markets.

Oil matters for FX because it feeds into several things at once:

- Inflation expectations

- Central bank pricing

- Current-account pressure

- Risk sentiment

- Commodity currency performance

- Emerging-market funding stress

That is what makes this story so important. A one-day spike in oil is manageable. A sustained risk premium in oil is different.

If oil remains high because shipping is constrained or investors demand a larger geopolitical premium, the FX impact becomes more serious. Energy importers come under pressure, inflation-sensitive economies become more exposed, and central banks may have less room to ease even if growth starts to slow.

That is a difficult mix.

It can support the dollar at times, but it can also create cross-currency opportunities where some economies are clearly more exposed than others.

The US dollar is still important, but it is not a one-way trade

The first instinct in a geopolitical shock is usually to buy USD.

That makes sense. The dollar is the world’s main reserve currency, it is highly liquid, and it usually benefits when investors reduce risk.

But this situation is more complicated because the US is directly involved in the conflict. That means the dollar is not just a safe haven sitting outside the story. It is part of the story.

Reuters reported that the US military carried out retaliatory strikes against Iran after what it described as unprovoked attacks on US forces, while Iran accused the US of violating the ceasefire by attacking an Iranian oil tanker, another vessel and civilian areas near the Strait of Hormuz.

That creates a messier USD setup.

If markets focus on global stress, oil disruption and defensive demand, the dollar can still find support. But if markets start to see the situation as a direct US geopolitical liability, or if diplomacy appears to improve, the dollar may struggle to build a clean trend.

So instead of assuming “bad news equals stronger USD”, the better approach is to watch how the dollar behaves against different currencies.

USDJPY, USDCHF and USDCAD may all tell slightly different stories.

JPY and CHF are the cleaner defensive gauges

If the market turns properly defensive, JPY and CHF are still the two currencies to watch.

The yen is especially important because it sits at the intersection of three forces: safe-haven demand, Japanese intervention risk, and global yield moves. That makes it messy, but also very useful. If yen crosses start falling sharply, it usually tells us risk appetite is weakening.

AUDJPY and NZDJPY are particularly useful in this environment. They are not perfect, but they give a quick read on whether markets are still comfortable owning growth-sensitive FX against a traditional funding/safe-haven currency.

If AUDJPY and NZDJPY hold up while oil jumps, the market is probably still treating the situation as contained. If they break lower while oil rises and equities wobble, that is a much clearer risk-off signal.

CHF is cleaner in some ways. It does not have the same intervention drama as JPY, and it can benefit when investors want safety without leaning too heavily on the US dollar. In a situation where the US is directly involved, that matters.

EURCHF is worth watching. If it starts grinding lower, it would suggest European energy exposure and regional risk are becoming more important.

CAD may benefit from oil, but do not oversimplify it

The Canadian dollar is the obvious oil-linked currency to watch.

Higher oil can support CAD because Canada is a major energy exporter. But in this environment, it is not as simple as saying “oil up, CAD up”.

When oil rises because of stronger global demand, CAD usually has a cleaner positive story. When oil rises because ships are being attacked, ports are blockaded and the Strait of Hormuz is under stress, the signal is less clean.

That kind of oil move can hurt global growth sentiment. It can also boost the US dollar through safe-haven flows. So USDCAD can become a tug-of-war between oil support for CAD and risk-off support for USD.

That means CAD may not perform as strongly as oil alone would suggest.

The key is whether oil strength is being treated as a commodity tailwind or a global growth tax. Right now, it feels closer to the second one.

AUD and NZD are vulnerable if this becomes a growth shock

AUD and NZD are not direct winners from higher oil.

They are more sensitive to global growth, China sentiment, commodity demand and risk appetite. That means they can struggle if the market starts treating the Hormuz situation as a tax on global growth rather than just an energy supply issue.

This is where the distinction matters.

If oil rises but risk appetite stays firm, AUD and NZD may not suffer too badly. But if oil volatility rises, equity markets weaken and yen crosses start breaking lower, AUD and NZD can come under pressure quickly.

NZD may be especially vulnerable in a fragile global environment because it often behaves like a higher-beta currency when markets are nervous. AUD has some support from hard commodity exposure, but it is still not immune if the market becomes more defensive.

So for now, the better question is not “is oil higher?”

The better question is: “Is higher oil starting to damage risk appetite?”

That answer will matter more for AUD and NZD.

Emerging-market FX and carry are exposed

The other area to watch is emerging-market FX.

This kind of environment is not friendly for carry trades. Carry works best when volatility is low, investors are comfortable taking risk, and funding conditions are stable. A Hormuz shock is the opposite of that.

If oil volatility rises and safe-haven demand builds, high-yielding currencies can come under pressure even if their carry still looks attractive on paper.

This matters for currencies like MXN, ZAR, TRY, PLN and HUF. They all have their own local stories, but in a broad risk-off move, investors often reduce exposure first and ask questions later.

That does not mean emerging-market FX must collapse. It does mean the risk-reward becomes less forgiving.

Wide spreads, lower liquidity and headline-driven gaps can make these pairs harder to manage. In an environment where military headlines can hit at any moment, position size matters more than usual.

The market is cautious, not panicked

The important point is that this still does not look like an outright panic.

Oil is higher, but the FX response is not screaming full defensive liquidation yet. That could change if shipping disruptions worsen, the blockade expands, or the UN route collapses completely. But for now, markets still seem to be trying to separate contained military exchanges from a broader escalation.

That may be optimistic.

The risk is that each “contained” exchange increases the chance of a mistake. The US says it does not seek escalation, and Iran has said the situation has returned to normal, according to the latest Reuters update provided. But markets have heard that kind of language before. What matters is whether the next few sessions bring quieter shipping conditions or another round of retaliation.

For traders, the key is not to overreact to every headline, but also not to ignore the shift in regime.

The market has moved from “ceasefire holding” to “ceasefire under pressure”.

That is a meaningful change.

The Venca view

Our read is that this is now a fragile, headline-driven FX regime with a clear oil shock risk.

The US dollar can still benefit from defensive demand, but it is not a clean one-way safe-haven trade because the US is directly involved. JPY and CHF look like cleaner defensive gauges. CAD may get some support from oil, but only if the market sees the move as a commodity tailwind rather than a global growth risk. AUD and NZD are vulnerable if higher oil starts weighing on risk appetite.

The pairs to watch most closely are:

- USD/JPY

- EUR/CHF

- AUD/JPY

- NZD/JPY

- USD/CAD

- AUD/USD

- NZD/USD

For now, this is not a market where we would chase every move. The headline risk is too high, and the first reaction can easily reverse if diplomacy improves or if both sides try to contain the latest exchange.

But the bigger message is clear: Hormuz risk is back, oil is responding, and FX markets are starting to price a more complicated geopolitical backdrop.

Inside The Venca Report, we will keep tracking how this flows through our FX forecasts, macro dashboard and weekly technical views. In this kind of market, the headline is only the start. The real edge comes from understanding which currencies are absorbing the shock, which ones are benefiting from it, and which ones are simply being dragged around by noise.

Comments are closed