Every few months, markets rediscover the same lesson: when volatility rises, the US dollar still matters more than almost anything else in FX.

That does not mean the dollar always goes up. It does not mean every currency move is simply a dollar story either. But when traders are trying to make sense of higher bond yields, shifting central bank expectations, oil shocks, geopolitical risk, or equity market stress, the dollar usually becomes the first currency they look at.

That is why any serious FX view needs to start with the dollar, even if the actual trade idea sits somewhere else.

The easiest way to think about the dollar is as the market’s main pricing tool for global uncertainty. When the outlook is calm, investors are more willing to move into higher-yielding or growth-sensitive currencies such as AUD, NZD, CAD, and some emerging market currencies. When the outlook becomes less clear, capital tends to become more selective. Sometimes it moves straight into the dollar. Other times, the dollar only holds steady while risk currencies do the weakening.

That difference matters.

A “strong dollar” environment is not always obvious from the dollar index alone. You can have a period where DXY is range-bound, but AUDUSD, NZDUSD, USDJPY, or USDCHF are still telling a much more interesting story underneath the surface. That is why we track the broader FX setup inside the FX Forecasts section rather than looking at one headline index and calling it a day.

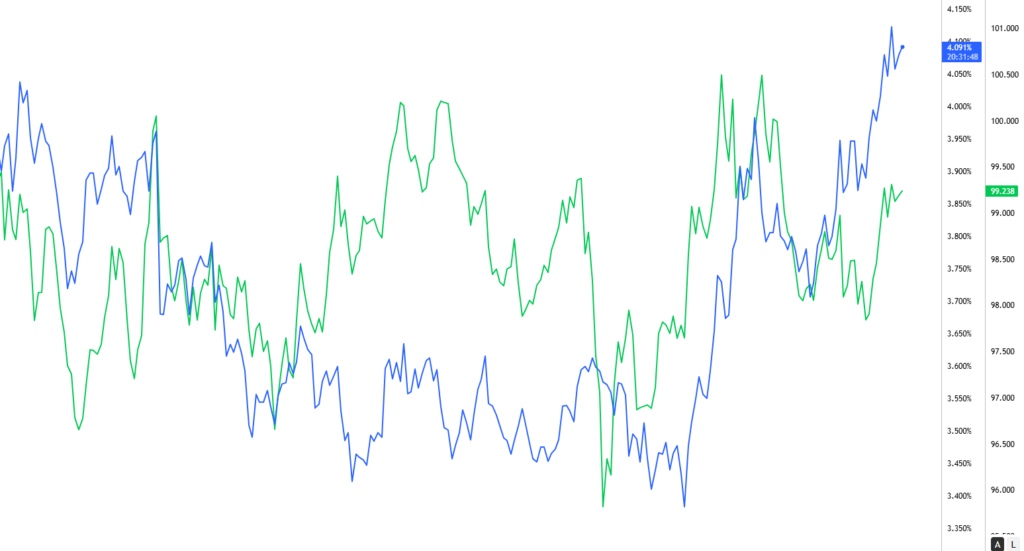

The first driver to watch is US yields.

The US dollar often tracks short-end Treasury yields because the 2-year yield reflects expectations for Federal Reserve policy. The relationship is not perfect, but when markets price a higher-for-longer Fed, the dollar usually receives some support.

When Treasury yields rise, especially at the front end of the curve, the dollar often gets support because investors are being paid more to hold US assets. This is not a perfect relationship, but it is one of the cleanest macro links in FX. If markets start pricing a more hawkish Federal Reserve, or simply remove expected rate cuts, the dollar can find a floor quickly.

That has been a recurring theme lately. Reuters reported that economists have pushed back expectations for Federal Reserve rate cuts, with many now expecting the Fed to avoid cutting this year as inflation pressure remains a concern. That does not automatically mean the dollar has to surge, but it does make it harder to build a clean bearish dollar view without strong evidence from growth, inflation, or risk sentiment.

The second driver is global risk appetite.

This is where FX gets more nuanced. In a classic risk-off market, the dollar, yen, and Swiss franc usually benefit, while AUD, NZD, CAD, and emerging market currencies come under pressure. But not every risk-off period is clean. Sometimes equities hold up while FX turns defensive. Sometimes the dollar rises because yields rise, not because investors are panicking. Sometimes the yen fails to rally because Japanese yield spreads are still working against it.

That is why the market cannot be reduced to “risk on” or “risk off.” It is better to ask: what kind of risk are we dealing with?

If the risk is growth-related, the dollar may gain because investors want safety. If the risk is inflation-related, the dollar may gain because US yields move higher. If the risk is fiscal or political, the dollar’s reaction can be more mixed. And if the shock is centered outside the US, the dollar can still benefit even when the US outlook is not particularly strong.

Oil is another piece of the puzzle.

Higher oil prices can support the dollar in some environments, especially when they push US yields higher or create stress for oil-importing economies. But oil shocks can also complicate the picture by hurting global growth and lifting inflation at the same time. That kind of backdrop can create uneven FX moves, where some currencies weaken sharply while others simply drift.

Recent market commentary has shown that oil and Middle East tensions have been major inputs for dollar direction, with traders watching energy prices, bond yields, and risk appetite together rather than in isolation.

For everyday traders and investors, the key point is this: the dollar is not just another currency. It is the center of the global FX system.

Before taking a view on EURUSD, GBPUSD, AUDUSD, NZDUSD, USDJPY, or USDCHF, it is worth asking a few basic questions.

Is the Fed becoming more or less supportive for the dollar? Are US yields rising or falling? Is the market rewarding risk-taking or punishing it? Are oil prices adding inflation pressure? Are investors moving toward safety, yield, or growth?

Those questions will not give the perfect answer every time. Nothing in FX does. But they will usually stop you from looking at a currency pair in isolation, which is where a lot of bad FX analysis begins.

This is also why we keep a close eye on broader macro themes inside the Macro Dashboard and pair-specific setups inside Weekly Techs. The best FX ideas usually come from combining both sides: the macro reason for why a currency should move, and the technical structure that helps with timing.

Right now, the dollar remains the currency that ties most of the major themes together. Yields, inflation, energy prices, risk sentiment, and central bank divergence are all feeding back into the same question: does the market still have a reason to hold dollars?

Until that answer becomes clearly “no,” the dollar will likely remain the main currency traders need to respect.

Comments are closed