China’s latest commodity trade data makes one thing pretty clear to me: we’re no longer in that simple “growth up, commodities up” world. Things are starting to split.

Energy is being driven more by supply security and logistics than anything else, while parts of the metals space are being held up by more selective forces – restocking, smelter behaviour, and pieces of policy support – rather than broad, clean end-demand. That matters, because it means you can’t just lump crude, iron ore, and copper together and assume they’re all responding to the same macro backdrop.

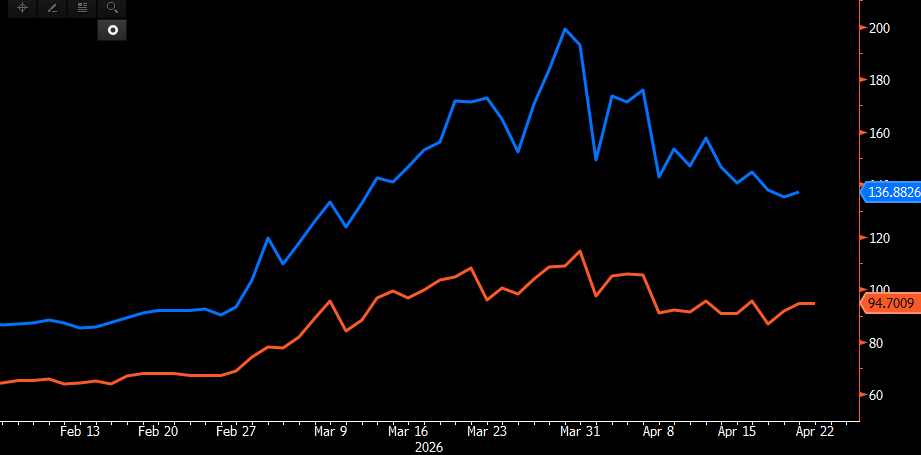

The March data really highlights that divide. Crude imports held up well, iron ore and copper concentrate demand stayed relatively firm, but natural gas softened and refined copper came under pressure. Same economy, very different signals.

The biggest driver sitting over all of this is still the disruption to Middle East energy flows. The Strait of Hormuz normally carries a huge chunk of global oil and LNG, so when that gets disrupted, the impact isn’t just on crude prices – it feeds through into freight, refining margins, and ultimately the cost and availability of key industrial inputs.

That’s why crude has held up better than many expected just looking at China’s import data in isolation. March imports were still strong, and more broadly, China looks to have been adding to inventories through Q1 while the rest of the world was drawing them down.

To me, that says less about booming demand and more about intent. China is prioritising energy security – locking in supply while it can – rather than reacting purely to price.

That dynamic creates a slightly awkward setup for oil in the near term. Stockpiles can smooth things out for a while, but they don’t solve the underlying issue. If imports start to slow and refined exports remain constrained, the pressure likely shows up in products – diesel, jet – rather than outright crude.

That’s already starting to come through. Product markets look tight and, if anything, that tightness will probably hold even if broader growth sentiment softens.

Gas is a slightly cleaner story. China’s imports have weakened, and LNG flows in particular have pulled back as buyers lean more on inventories, pipeline supply, and domestic production. At the same time, there’s been evidence of China reselling LNG cargoes into the regional market.

That’s quite telling. It suggests they’re not chasing spot cargoes aggressively at current prices, and that domestic demand isn’t strong enough to absorb everything. So while oil is being supported by strategic buying, gas looks more like a demand adjustment story.

In metals, things get a bit more interesting.

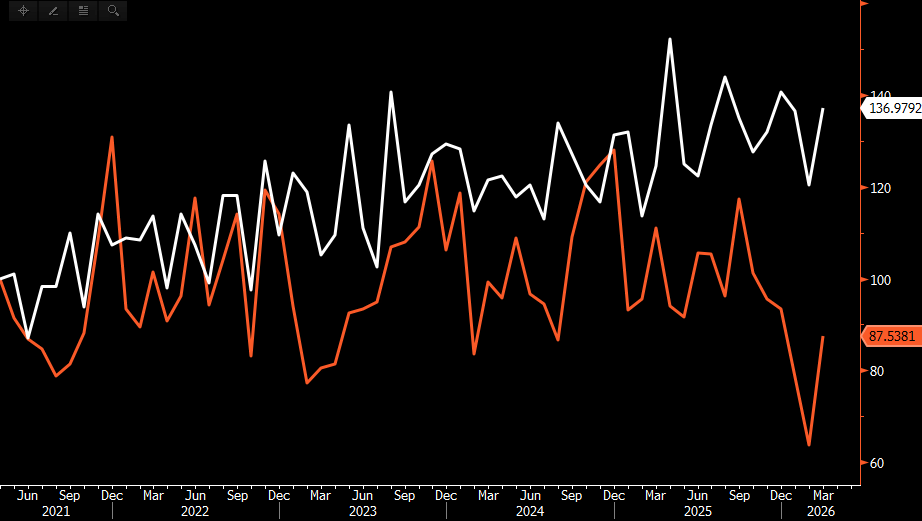

Refined copper imports have softened, but concentrate imports have held up. That’s a pretty important divergence.

It tells you that demand hasn’t just disappeared – it’s shifted. The upstream part of the chain is still relatively firm, while the downstream side is where the pressure is showing up.

At the same time, smelters are dealing with very poor economics. Treatment charges have been squeezed, but they’re still running, partly offset by sulphuric acid revenues. Add in the broader supply disruptions, and copper ends up sitting in a bit of a grey area.

It’s not a clean “sell China” trade, but it’s not a straightforward bullish story either.

My read is that copper probably stays messy for now. There’s a clear path higher if supply-side stress really bites, but without a stronger demand impulse, it’s hard to see a sustained trend just yet.

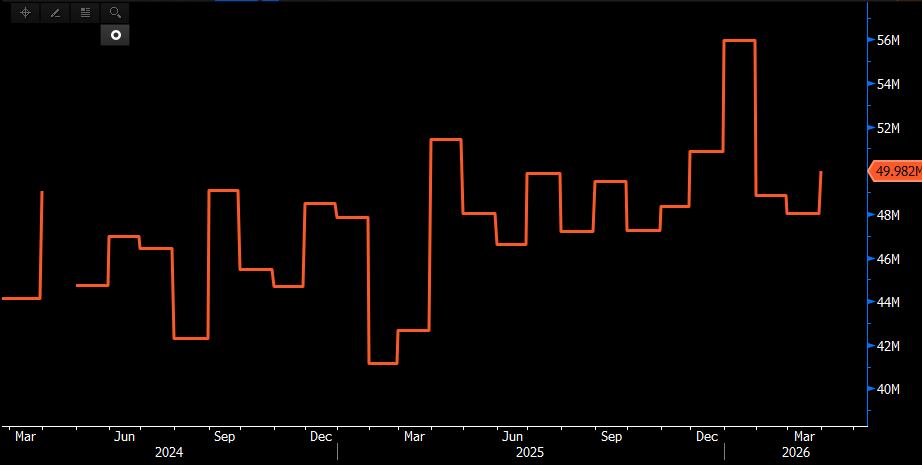

Iron ore, though, is probably the most misleading of the lot.

Imports have been strong – no denying that. But when you line that up against steel production, the story looks very different.

Steel output hasn’t really followed through in the same way, which suggests a chunk of that iron ore demand is coming from restocking or precautionary buying, rather than genuine end-demand.

That fits with the broader view. The steel sector is still dealing with structural issues – property weakness, excess capacity, and a reliance on exports and inventory management rather than a strong domestic recovery.

So while iron ore has held up better than expected, I’m a bit more cautious on the signal it’s sending. Strong imports doesn’t necessarily mean strong demand, and there’s a limit to how long that disconnect can persist.

Taking a step back, the bigger picture is that commodities are starting to fragment.

Energy – particularly anything exposed to shipping routes and supply chains – is being driven by security and availability. Bulk commodities like iron ore are being supported by inventory behaviour as much as demand. And base metals are sitting somewhere in between, caught between supply disruptions and patchy demand.

Right now, the “security of supply” side of that equation is winning.

My base case is that this continues over the next couple of months. Oil and products stay relatively firm, LNG remains tight but more demand-sensitive, copper trades choppy with upside risk tied to supply, and iron ore stays supported but struggles to push into a more convincing uptrend.

For that to change, you’d need either a clear de-escalation in the Middle East or a much stronger signal out of China on the demand side. Until then, it’s probably not a market where everything moves together – and that’s really the key takeaway here.

Disclaimer

The information provided in this article is for general informational and educational purposes only and does not constitute financial, investment or trading advice. The views expressed are the author’s opinions at the time of publication and may change without notice. They do not take into account your personal financial situation, objectives or risk tolerance.

Financial markets involve risk and past performance is not a reliable indicator of future results. Readers should conduct their own research and seek independent financial advice before making any investment or trading decisions.

The Venca Report accepts no liability for any loss or damage arising directly or indirectly from the use of the information contained in this publication.

Comments are closed